Introduction

The Finance Act 2022 was assented to by the President on the 21 st June 2022 and it contains the various tax measures and changes that will be applicable for the year of incomes 2022 -2023. Below is our summarized discussion of the various changes as well as their respective effective dates.

1. Income tax Act (ITA) Changes

1. Definitions of terms

Section 2 of the income tax act which deals with definitions of various terms as used in the main body of the Act has been amended by inserting new definitions. Fair market value and permanent home have previously been used in the Act but their definition had not been provided. This led to different interpretation by taxpayers. By adding these definitions, the Act seeks to bring the much needed clarity and will pre-empt any future tax disputes which could have arisen as a result of misinterpretation.

The Act further brings to tax the gains made from financial derivatives by non-residents and it was therefore prudent that financial derivate definition is provided. Below are the definitions as provided by the Finance Act:

- Fair market value – A comparable market price available in an open and unrestricted market between independent parties acting at arm’s length and under no compulsion to transact.

- Financial derivate – A financial instrument whose value is linked to the value of another instrument in a transaction to be settled at a future date

- Permanent home – A place where an individual resides or is available to that person for residential purposes in Kenya or where the individual’s personal or economic interests are closet.

The above amendment is effective 1 st July 2022.

2. Taxation of gains from financial derivatives

The Act has amended Sections 3, 9, 34, 35 as well as the third schedule. This effectively brings to tax

the gains made by a non-resident person who enters into a financial derivate contract with a resident person. The rate of tax will be at 15% and the resident person will bear the responsibility of withholding the taxes upon payment of the gains to the non-resident. However, derivate traded in the Nairobi Stock exchange have been exempted from tax. We expect the cabinet Secretary for the National Treasury to issue regulations before commencement of this Section.

Effective date: 1 st January 2023

3. Foreign Exchange Losses

Any company whose gross interest payable to related entities or third parties exceeds thirty (30) per cent of the company’s EBITDA (Earnings, Before, Interest, Tax, Depreciation & Amortization) will be required to defer and not claim foreign exchange losses arising from such loans effective from 1st July 2022. The Act further exempts microfinance institutions as licensed under the Microfinance Act,

2006 and any other entity licensed under the Hire Purchase Act.

4. Digital Service Tax

The 2022 Finance Act has exempted non-resident persons with permanent establishment in Kenya from the provisions of the digital service tax. Going forward, any taxes due and payable by the nonresidents persons will be accounted for under income tax. This is effective from 1st July 2022.

5. Expenses allowable for tax

Beginning 1st January 2023, the following expenses will be allowable deductions in arriving at the income chargeable to tax:

- Donations – Previously only donations made to organizations registered or exempt from registration under societies Act or the non-governmental organization Act were allowable for tax purposes. Going forward all donations made to any charitable organization will be exempted from tax. Further donations made to project approved by the Cabinet Secretary to the National Treasury will also enjoy the same status.

- Interest restriction – The following institutions will now be exempted from the interest restriction rule set at 30% of EBITDA. They will now enjoy a full deduction of interest on their income as is the case with financial institutions.

a) Microfinance Institutions licensed and non-deposit taking microfinance business under the Microfinance Act, 2006;

b) Entities licensed under the Hire Purchase Act;

c) Non deposit taking institutions involved in lending and leasing business;

d) Companies undertaking manufacture of human vaccines

e) Manufacturing companies whose cumulative investment is at least five billion shillings. The investment should have been made outside Nairobi and Mombasa City county.

6. Ascertainment of gains and profits of business in a preferential tax regime

Effective 1st January 2023, gains made by a resident person who carries on business with a non-resident individual located in a preferential tax regime shall be deemed to be those amounts which could have been expected had the transaction been conducted by independent persons dealing at arm’s length. Special Economic Zones and Export Processing Zones are examples of such regimes. The Commissioner has been granted powers to revise/ensure such transactions meet the arm’s length principal.

7. Multinational Enterprises

The Income Tax Act has been amended by inserting new sections which brings new requirements for multinational enterprises with regards to country by country reporting. This brings enhancement and the much needed clarity to the various amendment already introduced by the previous Finance Acts.

Below are highlights of the amendments which will take effect from 1st July 2022.

1. Multinational enterprises to notify the Commissioner not later than the last day of the financial year whether it is the ultimate parent entity or surrogate parent entity or the identity of the constituent entity if it is neither the parent nor surrogate;

2. Multinational enterprise with gross turnover of 95 billion to file a country by country report with the commissioner as well as file a master and local file;

3. The information to be included in country by country report, master and local file including due dates;

4. Offenses and penalties for failure to file the various returns/files with the commissioner; and

5. Provision in relations multinational enterprises will be applicable from the year of income 2022 onward.

8. Capital Gains Tax

The Finance Act, 2022 has amended section 34 1 (J) of the income tax Act so as to increase the rate of tax from 5% to 15%. This is aimed at aligning the Kenyan CGT rate with other EAC member states as currently Kenyan rate still remains the lowest in the region and to also tap on the tax revenues in the real estate sector which has experienced considerable growth over the years. This provision will take effect from 1st January 2023. However, any investment made prior to 1 st January 2023 and valued at KES 5 Billion will attract CGT at 5% where applicable.

9. Exempt Incomes

The Finance Acts 2022 has amended the first schedule of the Income Tax Act effectively exempting the following incomes from taxation. This will take effect from 1st July 2022.

1. Deemed interest in respect of an interest free loan advanced to a company manufacturing human vaccine;

2. Compensating tax accruing to a company manufacturing human vaccine;

3. Dividends paid by a company manufacturing human vaccine;

4. Income of a company manufacturing human vaccine

5. Dividends paid by Special Economic Zone enterprises, developers and operators licensed under the Special Economic Zones Act; and

6. Dividends to any non-resident person by Special Economic Zone enterprises, developers and Operators

10. Independent power producers

Effective 1st July 2022 machinery used for generation, transformation and distribution of electricity by independent power producers will henceforth be eligible for investment deduction allowance. Before it was only limited to those supplying power to the national grid.

11. Tax Incentives

The Finance Act 2022 has introduced reduced corporation tax rates for the following entities. This change will take effect from 1st July 2022.

1. Companies operating a carbon market exchange or emission trading system certified by the National International Financial Centre Authority will now be taxed a t 15% for the first 10 years upon commencement; and

2. Company undertaking shipping business in Kenya will be taxed at the reduced rate of 15% for the first 10 years upon commencement of the shipping business.

12. VAT Changes

Below are the changes to the various sections of the VAT Act, as contained in the Finance Act, 2022

1. Section 5 of the value added tax has been amended to reduce the rate of tax of liquefied petroleum gas including propane from 16% to 8%;

2. Section 10 has been amended to exclude suppliers who provide services over the internet from reverse VAT;

3. Section 22 amended to bring penalties and interest levied with regards to imported goods under the ambit of TPA, 2015. Previously these were levied as provided for in the EACCM Act, 2004. In duplum rule to apply; and

4. Section 30 which was dealing with refunds of taxes paid erroneously has now been repealed. Refund of taxes paid erroneously will henceforth fall under the TPA, 2013;

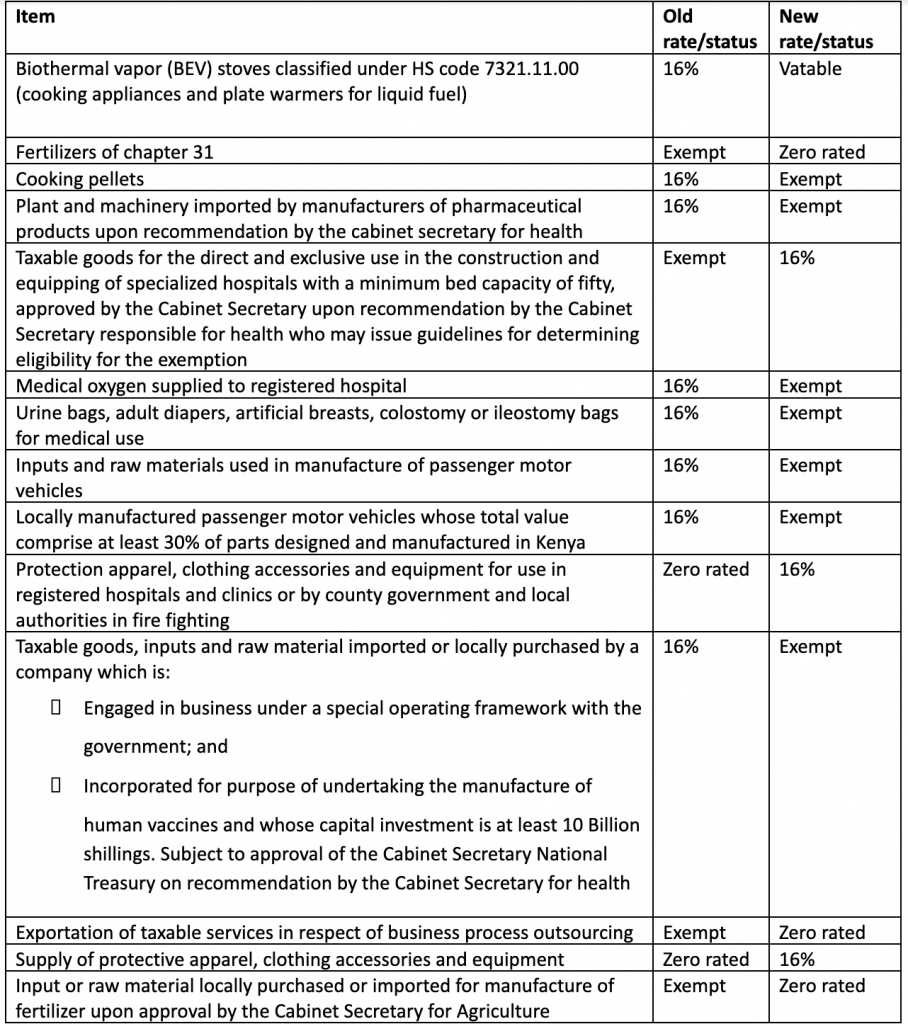

Changes to the first and second schedules of the VAT Act in relation to various goods and services

13. Tax Procedures Act (TPA), 2013 changes

The Finance Act 2022 has introduced the following amendment to the TPA, 2013 so as to streamline it to the various tax legislation and give the Commissioner powers to attach property for taxpayers who fail to pay taxes.

1. Section 31 of the TPA is amended to provide a six month time limit of claiming of input VAT. This is with effect from 1 st July 2022;

2. Effective 1 st July 2022 the Commissioner has been granted powers to attach properties situated in Kenya as security for unpaid tax upon notifying the Registrar in writing. Property has been defined to include land, building, aircraft, ship, motor vehicle or any other property the Commissioner may deem sufficient.

3. TPA has been amended by deleting section 47 and replacing it with a new section. This section deals with offset or refunds of overpaid tax. The amendments are to enhance and streamline the current procedures in relation to refunds or offset of overpaid taxes with regards to the various tax legislations. This will take effect as from 1 st July 2022.

4. The Commissioner is required to notify a taxpayer within fourteen days that their notice of objection has not been valid lodged.

14. Excise Duty Act Changes

The Finance Act 2022 has introduced various amendments with regard to how Excise duty is to be administered in Kenya. Below are the summaries of the highlights;

- Commissioner is given the power to exempt specified products from inflationary adjustment through a notice in the Kenyan Gazette;

- Penalties and interest as levied in the Excise Act will now fall under the ambit of the Tax Procedures Act. In duplum rule to apply; and

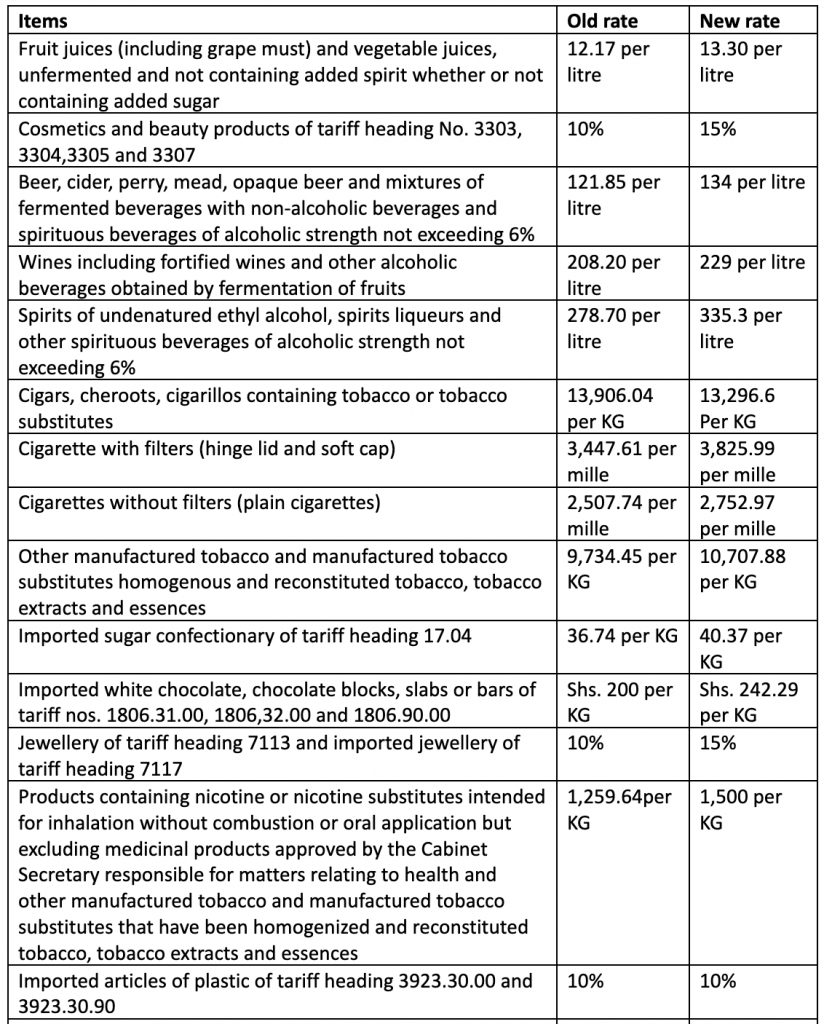

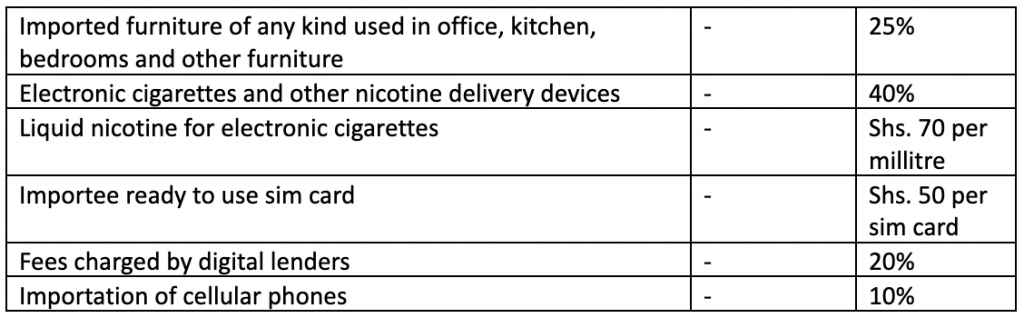

- Introduced the following rates in relation to the below goods and services.

15. Exempt excisable goods

The second schedule of the Excise Duty Act, 2015 has been amended to exclude the following goods from excise duty.

- Neutral spirit imported or purchased locally by registered pharmaceutical manufacturers upon approval by the Commissioner; and

- Locally manufactured passenger motor vehicles.

Disclaimer

While we have taken care to prepare the above information, the same should be used for guidance purposes only. Adequate professional advise should be sort where needed. The firm will not take any responsibility for any decision made based on the above information.

Team

For any clarification on the above kindly contact our Tax Service members on the below contacts:

Jeremiah Mvera – Tax Manager

T: 254 724 814 751

E:JMvera@mgkconsult.co.ke

Bearice Kamau – Tax & Outsourcing Partner

T: +254 721 281 430

E: BKamau@mgkconsult.co.ke

Share this: